July 2026

Swift goes live with payments scheme to tackle cross-border payments’ last-mile challenge

As cross-border payment volumes shift towards faster, more transparent alternatives, banks are under pressure to modernise their offerings. The new Swift payments scheme is designed to raise service standards on today’s rails – and Deutsche Bank is among the leading banks going live in its first phase

In cross-border payments, the last mile remains the biggest source of friction. Swift data shows that up to 80% of delays occur after a payment has left the Swift network – on the final stretch to the beneficiary account. This is where local clearing systems, rules and market practices introduce delays and uncertainty. Costs also remain hard to predict, with a US$200 cross-border remittance at around US$12 on average.1

The new Swift payments scheme is designed to tackle these issues. It introduces a common, rulebook-based framework across participating banks – setting commitments on upfront fees and FX transparency, full-value delivery, end-to-end tracking and the fastest possible settlement where domestic infrastructure allows.

In addition, the scheme places strong emphasis on straight-through processing (STP) and upfront data validation, helping to reduce manual intervention and improve processing consistency across the payment chain. Current service levels aim to achieve near real-time processing, with end-to-end delivery targeted within approximately 30 minutes where conditions allow.

“Deutsche Bank is helping to drive higher standards in cross-border payments by setting clearer service expectations and making delivery commitments more explicit for clients,” says Ciaran Byrne, Global Head of Product and Client Solutions, Institutional Cash Management, Deutsche Bank. “By combining our global network with ISO 20022 capabilities and APIs, we are improving transparency and predictability – while strengthening execution through higher STP rates, better data quality and faster, more reliable last-mile delivery.”

For end-customers, the scheme makes sending money across borders faster, more predictable and fully transparent. Hence, the scheme is closely aligned with the G20 roadmap for improving cross-border payments, which focuses on speed, cost, transparency, access and choice.

Deutsche Bank tests MVP with Westpac and Itaú

Officially launched in September 2025, the Swift payments scheme is now entering its second phase with more than 60 banks from 25 countries participating in the go-live of the minimum viable product (MVP). Deutsche Bank is one of the leading banks in this roll-out.2

“Even in these early stages, the scheme and the banks that are behind it are proving that we already have the technology available to provide end users with a fast, predictable and transparent international payments experience,” says Olivier Lens, Head of Central and Eastern Europe at Swift. “It’s an initiative that shows what we can achieve when we work together, taking us closer to the G20’s targets, but also allowing people to send money abroad with confidence.”

In mid-June, Deutsche Bank successfully completed its first live transactions under the scheme, demonstrating readiness across multiple corridors. Acting as gateway intermediary, Deutsche Bank processed cross-border euro payments into Germany from Australia (in collaboration with Westpac), and from Brazil (with Itaú), highlighting the scheme’s global reach (see Figure 1 below).

“For Westpac, the focus is on enabling our clients to benefit from a more predictable and transparent cross-border payment experience,” says Karen Ewens, Director, Network Management, Westpac. “Building on our initial deployments, we are continuing to expand the application of the Swift payments scheme with Deutsche Bank, helping to deliver more consistent and reliable outcomes for our customers across regions.”

“Participating in the Swift payments scheme is a natural extension of our client-centric strategy – ensuring that cross-border payments are not only faster, but also more reliable and aligned with our clients’ expectations,” says Gabriel Rombenso – Head of FX and Derivatives, Itaú. “By working closely with partners such as Deutsche Bank, we can combine strong data quality, automation and high STP rates to deliver a more consistent, scalable and end-to-end payment experience.”

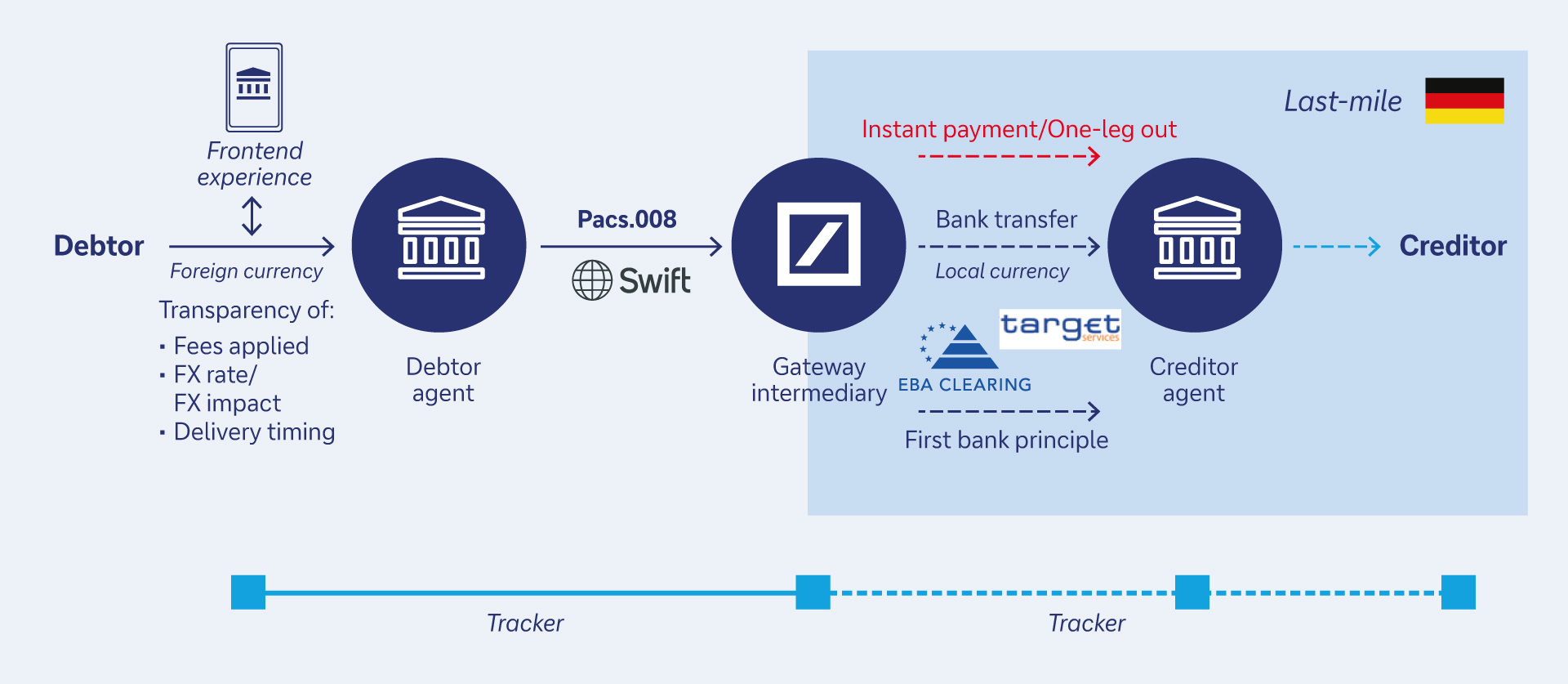

Figure 1: How the Swift payments scheme works

Source: Deutsche Bank

The gateway intermediary sits at the heart of the scheme’s last-mile execution. Positioned between the debtor agent and the creditor agent, it ensures payments are processed in line with scheme rules – supporting full-principal transfer, providing real-time tracking updates and enabling settlement via instant payment systems where available, or through book transfers to mimic near-instant cross-border payments.

The debtor agent is the financial institution serving the payer. It is responsible for the customer-facing initiation experience: capturing and validating the required data, checking payment eligibility, providing upfront transparency on fees, FX and expected delivery, and giving the payer visibility of the payment status.

What comes next

Deutsche Bank is initially focusing on euro inbound payments into Germany, leveraging its strong local clearing access and book-transfer capabilities. Further expansion –including additional corridors such as US dollar flows – is currently under evaluation as part of the next phase.

Following the MVP roll-out, Swift is aiming to further evolve the scheme, with an updated rulebook planned for December 2026 and a gradual expansion to around 300 banks across 30 creditor markets by 2027 – highlighting the scale of ambition behind the initiative.

Sources

1 See Cross-border payment technologies: innovations and challenges at bis.org

2 See Deutsche Bank, Swift and Financial Institutions Worldwide Team up to Deliver a New Era of International Money Transfers to Germany at businesswire.com